(Please note this article is for educational purposes only, I am not a financial advisor, this is not financial advice)

Introduction:

It’s impossible to predict big crashes in the stock market, right? Economists consistently get recessions wrong, move the goalposts, and scare you into believing the end is nigh. Then, suddenly one day (like in 2008), the world caves in, the markets are in turmoil, retirement plans go up in smoke, countless jobs are lost, and a generation is forever crippled by a “Great Depression” or “Great Recession”.

But what if I told you that this is all completely predictable, that you could in fact “time the market” (to a certain degree) and that you could use Cycle Theory to alter your path in life. Maybe not buy a house just before a huge downturn? Maybe not invest in a stock right at the top of the market. Well, it’s not a fantasy, in fact, it’s a reality, but few people know about it and even fewer believe it once they do know about it. Many, in fact, who are in the know just bat it away as hoodoo. And yet, these cycles have been going on for (in some cases) more than 200 years. Better yet, it’s incredibly simple to get your head around, and I am a testament to that. I am not an award-winning economist, nor did I study finance of any form at university. I’m just an investor who loves patterns and wants to not get burned any more. You don’t even have to take my word for it; there are a growing number of works highlighting this pattern including a wonderful one by Akhil Patel called “The Secret Wealth Advantage”. More on Akhil later no doubt, either in this post or future ones.

So, without further ado, let’s dive in.

Let’s lay a base:

To lay the groundwork, we first need to understand the basics. Economic cycles happen; they stand at the intersections of history and shape what happens in our world, in our societies and, in some extreme cases, the very environments we find ourselves in. The very idea of a cycle comes about due to things repeating in a certain way; they don’t have to be exact (in economic terms that would be very hard to achieve) but they will often rhyme. This rhythm, especially when looking at financial markets, is often known as “boom and bust”. When I think of booms, I think of the roaring twenties (1920s) or the boom period that led to the bust of the dot com bubble. Once you start to see these patterns emerge, you can, if you have an incredible understanding, even predict the next boom and the next bust. Samuel Benner, a 19th-century farmer turned economic forecaster, laid the groundwork for understanding these cycles through his observations of commodity prices and business conditions. His work, along with the subsequent theories of Nikolai Kondratiev and others, has illuminated the inherent ebb and flow of economic activity, often linked to underlying factors such as technological innovations, commodity prices, and broader socio-economic trends.

I will likely dedicate a post to each of these brilliant minds at some point, mainly so I can have them as touchpoints in the future, but for now, let’s press on.

I want to explore the predictive power and limitations of these economic cycle theories, particularly focusing on the anticipated market peak in 2026, followed by a downturn in 2027/28, and a prolonged bear market. Drawing on historical precedents such as the Panic of 1819 and the Great Depression, Benner’s own predictions amongst other markers that we can draw upon to aid in the idea of a painful upcoming crash in 2027/28.

Historical Context and Theoretical Foundations:

A. Samuel Benner’s Pioneering Observations

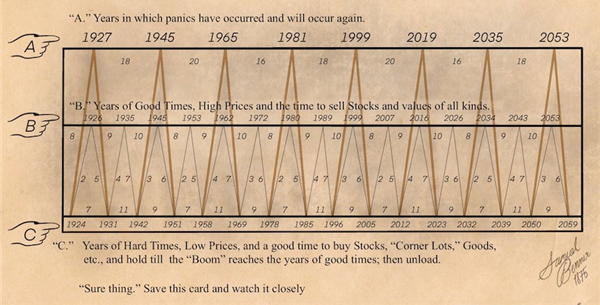

Samuel Benner’s foray into economic forecasting emerged not from academic inquiry but personal adversity following the 1873 market panic. As a farmer, Benner experienced firsthand the devastating impact of these economic downturns. His subsequent book, published in 1875, was an endeavour to make sense of the seemingly chaotic market forces. Benner’s approach was grounded in his observations of agricultural commodities, primarily focusing on pig iron, corn, and hog prices. He posited a cyclical pattern in these commodities, driven by natural rhythms and market reactions.

Benner’s work was pioneering in that it recognised the existence of predictable patterns within what appeared to be market chaos. His identification of panic years, periods of prosperity, and times of hardship laid the groundwork for the understanding that markets, much like agricultural cycles, are subject to predictable forces over time.

The image below is Benner’s Cycle. Bear in mind this was his predictions before the 1900s even began, which blows my mind. As you study the image, notice some key “panic” dates. By selling your stocks in or around 1927, 1999, or 2019 for example, you would have avoided heavy downturns that included the COVID crash, the Great Depression, and the dot-com bubble. Not bad for a farmer in 1875. Buying, for example, in 2012 (line C in the chart) and selling in 2019 again, would have resulted in some fantastic gains.

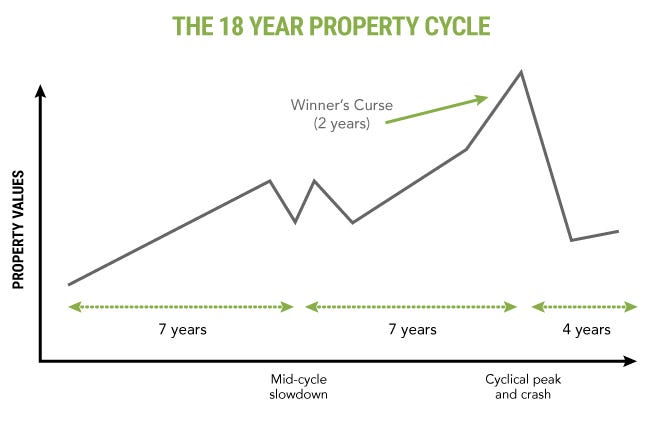

B. The 18.6-Year Real Estate Cycle

Building on the foundations laid by Benner, the 18.6-year real estate cycle offers a compelling lens through which to view market fluctuations. Phil Anderson’s work, notably in “The Secret Life of Real Estate and Banking,” delves into this cycle, demonstrating its persistent recurrence through history. The cycle, characterised by an average of 14 years of upward movement followed by approximately four years of decline, aligns intriguingly with the real estate peaks and troughs observed in historical data. This cycle’s predictability, as argued by Anderson, lies in the fundamental law of economics, drawing from David Ricardo’s Theory of Rent, which suggests that land value plays a crucial role in these economic swings.

C. The Kondratiev Wave and Broader Economic Implications

The long-term economic cycle, known as the Kondratiev Wave, offers a broader context for understanding these fluctuations. Spanning approximately 40 to 60 years, each Kondratiev Wave is thought to be driven by technological innovations and shifts in commodity prices, leading to alternating periods of prosperity and decline. This theory, while subject to debate among economists, provides a macroscopic view of economic cycles, encompassing the interplay between technological advancement, commodity markets, and global economic trends.

Economists have identified the following Kondratiev Waves since the 18th century:

- The first resulted from the invention of the steam engine and ran from 1780 to 1830.

- The second cycle arose because of the steel industry and the spread of railroads and ran from 1830 to 1880.

- The third cycle resulted from electrification and innovation in the chemical industry and ran from 1880 to 1930.

- The fourth cycle was fueled by autos and petrochemicals and lasted from 1930 to 1970.

- The fifth cycle was based on information technology and began in 1970 and ran through to the present day.

What is very interesting about this is that we are currently coming into the start of a new wave. We hit the 40-year mark around 2010, and the 60-year mark would obviously be 2030. We’ve just had (writing this in March 2024) the mass release of Artificial Intelligence. Its impact on our world and our society are totally unknown to us at this point, but could this be the next wave? I find it fascinating that this wave is lining up so nicely with Benner’s Cycle and the 18.6-year property cycle, not to mention the 100-year anniversary of The Great Depression when we saw mass unemployment, something which undoubtedly many are worried about with the rise of AI.

D. Linking Theory to Practice: Real World Implications

The theories proposed by Benner, the observations around the 18.6-year real estate cycle, and the Kondratiev Wave all converge to suggest that economic cycles, though complex, are not entirely unpredictable. This predictability, or at least the notion of it, has profound implications for investors, policymakers, and businesses. Understanding these cycles can potentially guide strategies for capital protection, investment timing, and policy formulation. However, this understanding also comes with the caveat that historical patterns, while indicative, are not foolproof predictors of future market behaviours, which is where I need to be careful and make sure I not only understand the cycles but understand when and why they might eventually break.

E. Setting the Stage for the 2026 Peak Prediction

As we approach the midpoint of the current 18.6-year cycle, with the backdrop of the COVID-19 pandemic and its significant economic impacts, the stage is set for the next market peak, anticipated around 2026. This prediction draws on historical patterns, particularly the real estate cycles, and aligns with the larger framework of economic cycles discussed.

The Mechanics of Market Cycles: From Expansion to Contraction

Understanding the intricacies of the 18.6-year real estate cycle, especially as we approach the anticipated market peak in 2026, requires a deeper examination of the cycle’s components. This cycle, eloquently described by Phil Anderson, alternates between roughly 14 years of expansion and 4 years of contraction. The expansion phase is characterised by a steady increase in market activity, including rising property prices, escalating investment, and a general atmosphere of economic optimism. Notably, this phase often includes a mid-cycle slowdown, serving as a brief respite rather than a complete halt in growth.

As the cycle progresses, the market approaches what is often described as the “Winner’s Curse” phase. Here, the investments and valuations made at the height of the expansion phase begin to show their fragility. This phase culminates in a market correction, leading to a downturn or crash and, subsequently, an economic recession. The historical pattern of this cycle, evidenced by past real estate peaks such as those in 1973, 1989, and the build-up to the 2007 global financial crisis, demonstrates a remarkable adherence to this 18.6-year rhythm.

The pig iron cycle, reflecting broader industrial and economic trends, serves as a microcosm of these larger market cycles. The progression from expansion to overproduction, followed by market saturation and eventual recovery, mirrors the larger economic health indicators. This cycle, therefore, is not only pertinent to the steel industry but also indicative of broader economic conditions, acting as a valuable gauge for industrial activity and potential shifts in the market.

In the modern context of a globalised economy, these cycles are no longer confined within national borders. The synchronisation of economic downturns and recoveries, as seen in the parallel experiences of countries like the U.S. and Australia, highlights the interconnected nature of global economics. The impact of international trade policies, global supply chain dynamics, and the role of multinational corporations are crucial in shaping these cyclical patterns.

As we inch closer to the predicted 2026 peak, monitoring various indicators becomes pivotal. Key factors to watch include real estate pricing trends, construction activity, consumer and corporate debt levels, and commodity market movements. Moreover, technological advancements and geopolitical developments could significantly influence the cycle’s trajectory, potentially altering its course or intensity.

In anticipation of this 2026 peak, the convergence of historical patterns and contemporary economic indicators suggests a cautious approach for investors, policymakers, and businesses alike. The lessons drawn from past cycles, especially when viewed through the lens of modern economic dynamics, provide invaluable insights for navigating the potential market fluctuations ahead. These insights not only aid in understanding what to expect but also in preparing strategic responses to mitigate the impacts of the predicted downturn.

Anticipating the 2026 Peak:

As we navigate towards the projected 2026 market peak, a confluence of factors, both historical and contemporary, shapes our expectations and strategies. The lessons of past cycles, particularly those observed by Samuel Benner and the consistent patterns in the 18.6-year real estate cycle, suggest that the upcoming peak could be precipitated by a combination of overvaluation in key markets, excessive credit expansion, and possibly, speculative investment behaviours mirroring those seen in previous cycles. This cycle will also include the rhyme of The Great Depression’s 100-year anniversary and Kondratiev wave beginning a new cycle. All these cycles do appear to be colliding into potentially “One Big Crash”. Equally, I don’t want to rule out the idea of “One Big Downturn” with no “crash” in sight, whereby we get a sustained, hard and long bear market, the likes of which our generation (I’m in my 30s) has never seen.

Potential Triggers and Economic Indicators:

The triggers for the 2026 peak might not be singular but a complex interplay of factors. High real estate prices and aggressive investment practices, reminiscent of previous cycle peaks, are likely to be among the key indicators. Additionally, technological advancements and evolving global trade dynamics could contribute to this culmination. The pig iron cycle, as an industrial barometer, might reveal early signs of overproduction and saturation, signalling an approaching market correction.

During my research, I wanted to see if I could predict this downturn by combining different sectors and different stocks. This is where things have gotten interesting for me.

The chart below is something I constructed over a year ago now and is a combination of housing stocks and building stocks. As these are publicly traded companies, I needed to carefully select these so that I could get a chart that went back pre the 2000s, just to make sure I was getting as good a dataset as possible. There are also more stocks that you can add to this to enrich this data and continue to support the overall chart, but they can only be used after 2000.

This chart, however, appears to highlight a topping pattern before the dot-com crash

Stocks — DHI, TOL, LEN, PHM, KBH, LOW, CRH, VMC

In the first example, this series of stocks peaked in July 1998, 308 days before the general stock market reached its peak in March 2000. Then again, in July 2005, this chart showed a peak 700 days before the general stock market peaked in October 2007. Currently, as of March 2024, this chart appears to be nearing a peak, with a significant multi-year monthly bearish divergence occurring on the RSI. We might be witnessing the early stages of a downturn in the Property Market, with building stocks not performing in line with the broader stock market. If this pattern continues, we could see a market peak in mid to late 2026, aligning eerily with our early data points for Benner’s Cycle and the 18.6-year land and property cycle. If this chart plays out as I hope, it could act as a canary in the coal mine for future cycles, and it’s something I intend to monitor closely.

The analysis is not based solely on the charts but also incorporates knowledge of the 18.6-year cycle, with previous market crashes from 1987, 1990, 2000, and 2008. We can correlate this with the data from the home building stocks to begin plotting potential future crash points when these stocks start to decline again.

For example, a peak in home building stocks in March 1987 was followed 203 days later by a stock market crash, and a peak in October 1989 was followed by a crash 280 days later. A peak in July 1998 led to a crash 792 days later, and finally, a peak in July 2005 preceded a crash 1155 days later.

With data points of 203, 280, 792, and 1155 days, we have a limited dataset for predicting future crashes. However, we can observe that since 1987, our economy and stock market have grown considerably, correlating with an increased duration from the peak of home building stocks to a stock market crash.

Based on the current trends, one could speculate that once the building stocks peak (which as of March 2024 hasn’t happened yet), we might see a stock market crash between 1200–2000 days later. This prospect is intriguing, as this dataset will expand with each occurrence.

If, as of writing this in March 2024, we have seen these stocks peak, we could anticipate a crash anytime between May 2027 and August 2029.

B. The Impact of a Prolonged Bear Market Post-2026

The aftermath of the 2026 peak, assuming historical patterns persist, could be a prolonged bear market starting in 2027/28. This period would likely be characterised by reduced consumer spending, slowed economic growth, and possibly higher unemployment rates. The downturn would impact various sectors, notably real estate and commodities. The extent and duration of this bear market could be influenced by responses in fiscal and monetary policy, geopolitical events, and the global economy’s ability to withstand shocks. Should all these cycles converge, we could witness an unprecedented economic scenario.

Based on Benner’s Cycle, re-entering the markets might not be advisable until 2032, indicating a significant downturn. However, given the current observations, this seems plausible.

C. Strategic Preparations and Mitigating Risks

For investors, comprehending these cyclical patterns is vital for strategic positioning. Diversifying portfolios, emphasising long-term value over short-term gains, and ensuring liquidity are wise strategies as the market approaches its peak. Businesses should aim to strengthen their balance sheets, manage debt levels, and prepare for a potential dip in consumer demand.

Policymakers face the challenge of enacting regulatory measures that moderate market excesses without hindering economic growth. Insights from past downturns, emphasising the importance of timely and targeted fiscal stimuli, could guide efforts to lessen the severity of the post-peak recession.

Unfortunately, policymakers often either misunderstand the 18.6-year cycle or choose to overlook it. It’s likely we’ll witness further bank bailouts, increased currency debasement, and more challenges for ordinary workers, while measures to stimulate the economy could initiate another 18.6-year cycle in the 2030s.

My conclusion:

I believe we are rapidly approaching an economic turmoil unlike any I have seen before. This could be a disaster on the scale of 2008, potentially worse, unfolding slowly. The convergence of the cycles discussed in this post at what seems like the worst possible time is particularly concerning.

The critical question for me is how to mitigate the worst effects and position myself to capitalise on the opportunities that arise. The forthcoming downturn presents a chance to acquire assets such as property, stocks, gold, and bitcoin at significantly reduced prices. Successfully navigating this “Big Crash” could set a foundation for lifelong financial security.

Originally published at https://www.wordsbysimon.com on February 8, 2024.